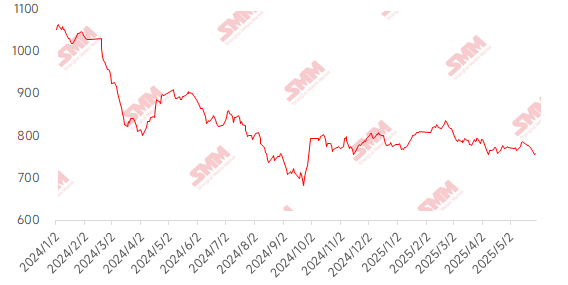

This week, the prices of imported iron ore first declined and then rebounded. During the Dragon Boat Festival holiday, the US White House announced that it would increase tariffs on imported steel, aluminum, and their derivatives from 25% to 50%. This news heightened market concerns about the uncertainty of steel exports, leading to the spread of pessimistic sentiment. However, as the US and Chinese heads of state held a phone call on Thursday night, releasing positive signals and confirming that the existing tariff policies would remain unchanged, market sentiment was significantly boosted. From a fundamental perspective, the supply side showed a contractionary trend, with global iron ore shipments and port arrivals declining simultaneously last week, and the supply increase falling short of expectations. The demand side remained relatively resilient. Although pig iron production continued to decline slightly, the absolute value still maintained a high level of over 2.4 million mt/day. Coupled with the continuous slight destocking at ports, the supply-demand pattern supported prices. Under the dual influence of easing macro policies and fundamental support, iron ore prices completed the transition from weakness to strength, showing an overall pattern of fluctuating rangebound. In the spot market, the weekly average price of PB fines at Shandong ports dropped slightly by 7 yuan/mt MoM.

Chart-: SMM 62% Import Ore MMi Index

Data source: SMM

This week, domestic ore prices declined slightly, and it is expected that domestic ore prices will still have room to decline next week. In Hebei's Tangshan, Qian'an, and Qianxi regions, prices fell by 5-10 yuan/mt. In west Liaoning, prices in Chaoyang, Beipiao, and Jianping dropped by 1-5 yuan/mt. In east China, prices fell by 50-55 yuan/mt.

The supply and demand in the iron ore concentrates market in Tangshan, Hebei, were in a wait-and-see mode, with relatively stable prices. The dry-basis, tax-inclusive delivery-to-factory price for 66% grade iron ore concentrates was 920-930 yuan/mt. Overall market transactions were sluggish. Local independent beneficiation plants faced losses and shipping pressure, and production shutdowns for maintenance were common. The cost-effectiveness of domestic iron ore concentrates declined, and steel mills mainly purchased as needed. Amid weak supply and demand, there was no significant pricing activity in the market.

The domestic ore market in west Liaoning was sluggish. Affected by the price-driving actions of local leading steel enterprises and the continuous weakness of the market, the ex-factory prices of 66% grade wet-basis, tax-exclusive iron ore concentrates in the region were 690-700 yuan/mt. Currently, traders lack confidence in the future market and have low purchasing enthusiasm. Considering the limited profit margins, their offers are generally low. Mines and beneficiation plants, considering the relatively high cost support for iron ore concentrates, have temporarily halted shipments. Overall, market trading sentiment is weak.

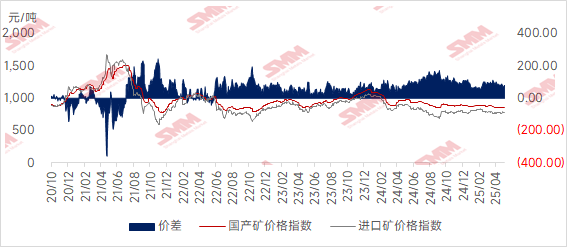

Most mines and beneficiation plants in east China are operating normally as planned, but recent shipping conditions have been average. The cost-effectiveness of domestic ore has shown a weakening trend, and overall market transactions have been relatively sluggish. From a pricing perspective, the average price index of imported ore this week declined slightly WoW, and it is expected that local iron ore concentrate prices will still have some room to decline.

Chart: Price Spread Between Imported and Domestic Ores

Source: SMM

Outlook for Next Week

Imported Ore Perspective: Looking ahead to next week, the iron ore market is expected to exhibit a pattern of weak supply and demand, yet with underlying support remaining. From the supply side, despite the anticipated rebound in global shipments, the efficiency of port operations will be significantly constrained by the persistent heavy rainfall in South China, and the actual port arrivals are expected to remain at a low level. On the demand side, influenced by seasonal maintenance, the operating rate of blast furnaces at steel mills may continue to drop back slightly. However, considering that pig iron production will still be maintained at a relatively high level of over 2.4 million mt/day, the support from end-use demand for ore prices remains strong. From a macro perspective, with the marginal easing of Sino-US tariff issues and the rising expectations for domestic growth-stabilizing policies, particularly the potential support measures in infrastructure investment and consumption stimulus, the market's risk appetite is expected to improve further. Overall, driven by multiple factors such as short-term supply constraints, persistent demand resilience, and an improved macro environment, iron ore prices are expected to fluctuate upward next week, with room for a slight rebound.

Domestic Ore Perspective: In summary, the supply of domestic iron ore concentrates remains tight. However, influenced by cost-effectiveness, steel mills are mainly purchasing as needed, leading to weakened demand. Coupled with the recent weak trend in the iron ore futures market, it is expected that the prices of domestic iron ore concentrates may have some room to decline.

》Click to View SMM Metal Industry Chain Database

![[SMM Steel] MMK Metalurji halts output in Turkey amid wage dispute](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)

![SMM Steel] EU sets CBAM certificate price at €75.36/t CO₂ for Q1 2026](https://imgqn.smm.cn/usercenter/aPBtI20251217171717.jpg)

![[SMM Steel] Steel market outlook improves amid policy support and tighter supply](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)